How to tackle the tax issue for your business

Apr 11, 2017

Financial Vehicles- 04 Taxes from Overflow on Vimeo.

_____________________________

I shot the video above with a friend of mine who's #CrushingIt in his insurance biz. He's been so successful that Farmers actually has him train others. So, I thought you'd benefit from his tips, as well as some of the info here I've pulled from The Field Guide to the Comp Plan.

* By the way, this video comes from the series, Financial Vehicles.

Anyway...

Happy to pay taxes?

A few months ago, a friend posted on social media that he was happy for tax day. It was April 15 and he couldn’t be more thrilled.

“I get to send another check to Uncle Sam,” he tweeted. Then- “#Grateful.”

Sounds strange, right? I mean, even in the Bible people hated tax collectors...

Why was he excited about paying more money to the government? Because he’d figured that the more he owed, the more he’d made. Face it, you're not going to dodge taxes. As someone said, there are two things that are certain in life: death is one, taxes are the other.

Once you resolve it in your heart that you are going to give some of your money back to the government (generally a certain percentage), you’ll figure out what my friend did. If you’re paying them more, that means that percentage equalled more… because as 21% (or whatever tax rate you’re paying) of something grows that means the 100% of that something grew, too.

In The Husband's Field Guide I introduced you to Les. I explained to him one day that Cristy had started getting checks that were somewhat significant in size, and that I was starting to budget and plan for a few things.

“We’re setting a specific bit of money aside for Cristy to put back into her business each month… and we’re putting a specific percentage aside for taxes…”

I explained, “I know you guys learned this through experience. You’re about 18 months ahead of us… I’d simply like to hear what you’ve learned and save myself the time trying to learn it. I’ll borrow your research and just do whatever you found out we’re supposed to do with taxes and everything…”

The same questions everyone has

Over the next few weeks, Les realized that many people were wondering what the next step was in this area of budgeting and financial planning. The result is that he planned a one-hour class and invited his accountant to come speak to the group. We sent questions to her ahead of time so she could come with prepared answers.

In one hour, she literally answered each of the following:

- What should I do to keep good records?

- What about your 100 PV / month requirement? Can you deduct this on taxes since it’s a required purchase in order to receive commission?

- What about the money we spend on samples and giveaways? Can and how do we deduct it?

- What are the best ways to write off your car, home office, and other expenses? What is the best way to track it all?

- What are the differences between standard and actual expense deductions?

- What classifies as a business trip? How long can you stay away before it becomes a “fun trip” instead of a working trip?

- Should I file and pay taxes quarterly? Or should I file annually?

- Employee vs. independent contractor? How do I know which one I’m getting if I’m hiring someone to help us in the office?

- What do I do if I pay my kids to do some things that help the business?

- What percentage of your commission check should you set back for income taxes?

- Should I set up an LLC?

- Where do most people leave “money on the table” that they could be putting in their pocket?

- What about business losses? How long do I have before I must show a profit to the IRS?

I know. That’s a lot of information. And I’m not going to run through it right here.

I can provide you with access to the answers, though. If you’ll listen to the “Tax talk with LaVana,” you can work your way right through the questions above in that order.

___________________

Here's her talk

___________________

By the way, Robert T. Kiyosaki, the author of Rich Dad Poor Dad, says this: “Money is one form of power. But what is more powerful is financial education. Money comes and goes, but if you have the education about how money works, you gain power over it and begin building wealth.”

Arguably, one of the biggest financial expenditures you'll make each year is your taxes. When your business starts booming, you’ll pay more in taxes than you pay on a mortgage, than you pay for a car… than you’ll pay for vacation. It only makes sense that you get a basic understanding of how taxes work.

Tax basics 101

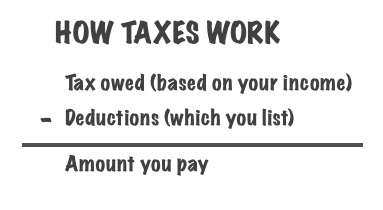

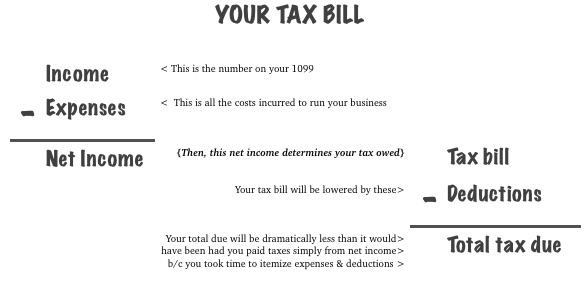

Here’s what I’ve learned: taxes are based on your income.

I know: you probably already knew that. After inputing your income into a form, the IRS tells you how much you owe. Then, they subtract any deductions that you have from that bill.

In other words, the equation looks something like this:

My advice is to to speak to a professional as soon as you consistently receive more than $1,500 / month on your commission check. And begin keeping records immediately. However, since I’ve got your attention for the moment, I”ll give you some basics to help you understand the equation above.

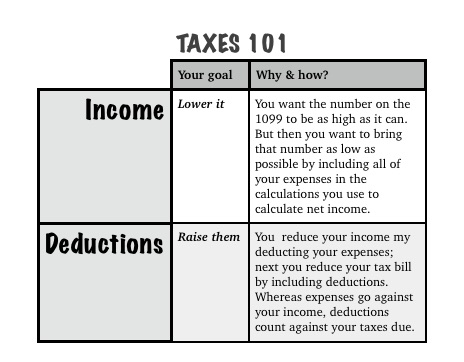

First, let’s talk income

You will receive a 1099 this year if you earn any commissions from your business. That’s why they take your Social Security number.

Basically, a 1099 means that no taxes have been withheld from your earnings. The form simply reports to the IRS the amount of monies you received as income during the previous year.

Young Living will send you a 1099 that has at two potential sources of income on it:

- Your monthly commissions will be on the 1099. You were expecting to see this.

- Any trips or prizes you won… will also be on the list. You might not have expected this any more than I expected to see an itemization for the trips Cristy has won / earned over the past few years.

I’m certainly not complaining that we received an income assessment for the trips- any more than I would have complained if I won a Lexus or something else and had to report that as income. You wouldn’t complain, either. You just need to remember that Uncle Sam is going to want a share of it- and he will complain if he doesn't get a piece of what he thinks is his.

Here’s what you need to know…

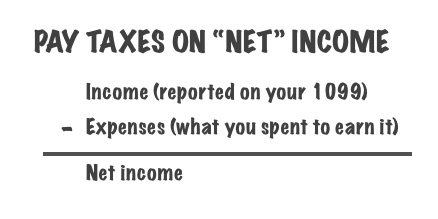

When it comes time to determine how much taxes you owe, you want to start by reducing your total income. No, I don’t mean that you should work less or intentionally sabotage your business. Or that you should use this as an argument to stop working before the end of the month (Like how I brought that one back into play?).

Earn as much as you can. Then after you earn it, be sure you leverage all of your business-related expenses to prove that everything reported to you on that 1099 was not “pure profit.” In other words, the income you received on your 1099 wasn’t free, so take out the costs related to earning that income.

Think about it. Even the trips Cristy wins aren't free. She spends a lot of money on marketing materials during those seasons, she drives a lot of miles, and she hosts several dozen people.

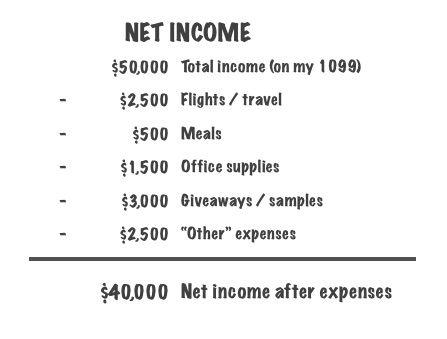

Let me show you what I mean. Let’s say I earned $50,000 last year. That’s the amount reported on my 1099. That’s income.

I don’t want to pay taxes on $50,000, because I had some expenses related to earning that income. That money wasn’t free. I had some legitimate expenses I incurred trying to get it.

Things like this:

- Let’s say I took a few flights (to convention and other business trips). Those flights cost me a total of $2,500. Now my net income is down to $47,500.

- I also had some business dinners last year totaling $1,000. For some reason, the IRS only allows you to count half of your meals, so this reduces my income by $500 more, bringing my income down to $47,000.

- I also had a home office. I bought pen and paper and print cartridges and other assorted supplies for a total of $1,500 / year. My income is now down to $45,500.

- In addition, I spent $3,000 on products to giveaway, as well as run promotions over the course of the previous year, bringing my income down to $42,500.

- I also spent $2,500 on “other” items. I didn’t know how to classify them. Some of these expenditures were marketing materials. Others were social events I did for my team. Some of these items included registrations to workshops and other events I attended. This dropped my income to $40,000.

Now, there are other expenses I can use to reduce my income. For instance, I stayed in hotels the times I flew out of town. And I had Internet service in my home for the entire year that I used for my business. I racked up a bit of a bill at the post office mailing books and products to team members. Oh, and I had a monthly iTovi fee. And all of those reference books that I gave away!

You see how this works?

I would rather receive a tax bill for $40,000 of income- or whatever that final number is by the time I take out all of my expenses- than for the $50,000 that’s reported on my 1099.

Yes, I want the number on the 1099 to be as high as it can. But then I want to bring that number as low as possible by including all of my expenses in my calculations I use to get to my net income.

Let me show you the math this way- straight from the numbers I gave you a moment ago.

Here’s how I've tracked all of this for our business:

The first few months I did this, I created a spreadsheet. I recorded everything by date on a single spreadsheet.

After a saw how much this adds up, I created a Quickbooks file and started running our finances like a legit business- just like I did when we began a nonprofit a few years ago.

In my opinion, using the software is easier, because it adds and subtracts everything for me. And, if you’ve set your categories up on the front end, it makes it easy to quickly review how much you’ve spent on a specific thing.

There are a few other things I do, as well:

- If it’s a business dinner, I record where it was (and include the address to add for mileage), and how much it cost. I toss the receipt in a file folder that I keep sorted by date.

- I also include dates and addresses when we drive to teach classes.

- If we purchase books to use as giveaways, I record it. If we sell some and recoup our expenses, I record that back as income.

At the end of the year, I have everything in one place.

You may want to work a system like I’m using, or you may opt for an app like TaxBot that you can run from your phone. At some point, when I’m not busy writing or wading through other projects, I intend to evaluate the swap myself.

Either way, you are not required to send the IRS all of your supporting documentation when you file your taxes (i.e., all of your receipts, mileage logs, etc.) You do need to keep them on file for a few years, however, so you have them if you are audited.

In the event of an audit, the burden of proof is on them- not you. However, things will go much smoother if you have a shoebox or folder with everything in it. By the way, digital receipts and photos of receipts are kosher, too.

Some people wonder if an LLC will help you with taxes. The short answer is “No,” because an LLC is a “pass through” organization. An LLC provides you with a layer of legal protection not “tax immunity.” And, when you file taxes for the LLC, the paperwork will declare who the members are- and then pass the income and subsequent taxes straight to them (read: you). If you’re going to use an LLC, then, understand that you are using it for legal protection not for tax abatement.

Second, let’s talk deductions

Your income minus your expenses gives you a better idea of your actual income. That “net” income used to derive your tax. Remember, in the example above we dropped my hypothetical income from $50,000 to $40,000.

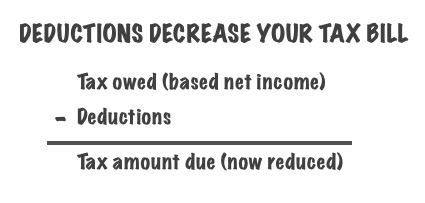

Now I owe taxes on $40,000 of income rather than $50,000. But I don't want to pay that bill… yet.

This is where deductions come into play. You can lower the amount of tax you owe by taking deductions that reduce the amount of your tax bill. It looks like this:

Let’s say the tax rate at $40,000 is 15%. (It’s not, but doing this with round numbers will be easier.) This means that I owe Uncle Sam $6,000 before itemizing my deductions. I have reduced my income my deducting my expenses; now I’m going to reduce my tax bill by including deductions. In other words, Whereas expenses go against your income, deductions count against your tax bill due.

Now, there are two ways you can count your deductions. You can take the standard deductions or the actual expense deductions.

- If you go standard deduction route, you’re agreeing to take the flat rate the IRS says you can take- like $5.00 / square foot for a home office or approximately $.50 mile for your car.

- If you go the actual expense route, you’re agreeing to keep up with the receipts and prove that you spent the money on that specific purpose (i.e., you count all gas receipts, repairs, oil changes, etc.- and then factor out what you used for personal driving).

We currently use the standard deduction method. The actual expense option seems more time consuming and burdensome. And, to be honest, on most days I already feel like a kite in a hurricane.

You’ll determine what’s best for you. Just know that you can’t swap back and forth. You’ve got to be consistent on the method you choose to report.

Understanding the difference between deductions and expenses can be confusing. For instance, the business dinner you enjoyed last week with your team member was an expense. It lowers your income. However, the baby sitter your hired to watch your kids while you were at that meeting is a deduction. It lowers your tax due. In my mind, this makes no sense- both items seem like expenses to me because I’m watching money go out of my hands in both cases.

There are numerous confusing items like this which is why it’s well worth it to get an accountant. Early in your journey, if you have good records, it will cost you a few hundred dollars to do this. It will be well worth it. They’ll likely save you more than the few hundred they cost, and they’ll represent you in the event of an audit.

Plus, you need to spend the mental energy running your business, not trying to manage tax issues. Face it, you’re a network marketing professional- not a CPA.

In the end, it’s helpful for you to have a basic understanding of how taxes work. Then I suggest you do the following:

- Keep great records, and

- Find a professional to digest the info and submit it to the IRS on your behalf.

Anyway, if we determine that I have $4,000 in deductions, all derived from baby-sitting, writing off the laptop I use for my business, taking into account my charitable giving, and my mileage I have reduced my tax bill from $6,000 to $2,000.

See how that works?

If I simply took the $50,000 as my total income and paid my tax bill from that (again, let’s just use that 15% for the sake of comparison- even though the tax rate is higher at $50,000) I would have paid $7,500 in taxes.

However, after reducing my income by accounting for all of the expenses I incurred related to earning that income and then obtaining a lower tax bill ($6,000) I itemized by deductions to reduce by bill even more.

Itemizing the deductions reduced my bill from $6,000 to $2,000- not bad considering I was originally looking at forking over 7,500 of my hard-earned George Washingtons.

Do these four things

Now that you know how this works, I suggest you do the following:

First, find a professional to assist you as soon as you are consistently receiving $1,500 or more on your commission check. You don’t need to do this on day 1 of starting your home-based business any more than you need to run out and create an LLC.

I hope you’re seeing that paying a professional a few hundred dollars will literally save you thousands as things progress. Plus, anything you pay them can be counted as an expense, and they’ll represent you in the event of an audit.

Second, begin keeping records immediately. You don’t want to pay out more than you have to when it comes time to dealing with Uncle Sam. If you haven’t been keeping records in the past, don’t worry about the past at this point. Get a good system and start today.

The recording and filing system you keep doesn’t have to be fancy- mine began as nothing more than the spreadsheet I keep on my computer and a few file folders.

Third, begin setting a percentage of your check aside each month now in a separate account so you can pay your bill next year. No matter how large or small the tax bill is, you don’t want to have to “lose a paycheck” by dedicating that entire check to your taxes next April 15.

Cristy and I started setting aside 23% earlier this year. After a while, we figured that was too high. Now, we set aside 20%. That’s probably a bit high for the place we’re in growth-wise and expense-wise (plus, we have a bunch of deductions), but we would rather have the money on hand and have some left over rather than saving too little and going to look for more.

Fourth, grab the free tools here that are available to you- including an audio file from a CPA, an ebook written by a former IRS trainer, and some other notes.

Disclaimer

Again, the purpose of this chapter is simply to provide you with an overview of tax basics as well as point you in the right direction. I’m not a CPA- or even good at math.

I’m evidently an entertainer of sorts, as evidenced by the fact that I got you to hang with me through a discussion on something you probably avoided or slept through while in school.

Watch the video above with David, and listen to the info from LaVana. Then, find a tax pro of your choice once you hit the $1,500 threshold, spreadsheet in hand.

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.